Every era of media has produced a new channel that brands eventually had to take seriously. Print and broadcast came first. Digital and social followed. What Charles Hambro, CEO of GEEIQ, argued at Advertising Week Europe 2026 is that virtual worlds are the third pillar in that progression, and most brand budgets still treat it as optional.

How Brands Measure Attention Today

Every major marketing channel has its own measurement language, and each has evolved alongside the medium.

Out-of-home advertising has been with us the longest. Measurement is built on footfall, traffic, dwell time, and estimated impressions, assessed through brand lift studies and, occasionally, search uplift when a creative lands hard enough to make people seek it out. The honest version of what a CMO presents to a CFO is estimated revenue, not direct attribution. Exposure is strong. Behavioural signal is weak.

Television extended that framework: gross rating points, reach, frequency, panel-based measurement from companies like Nielsen. The same brand lift studies and marketing mix modelling sit at the end of the attribution chain. The channel is trusted, recall impact is real, but direct attribution remains limited.

Both share a defining characteristic: they are passive experiences. The consumer is not choosing to engage with your brand. They are being interrupted by it.

Digital advertising changed the equation. Actual impressions, actual clicks. CTR, CPC, CPA, ROAS. The impact chain runs from impression to click to conversion to revenue, and a CMO could finally walk into a boardroom with direct attribution numbers rather than models. Social media continued the progression, stronger on user-level data, higher creative and cultural impact, and for the first time, the ability to own an audience without paying for every reach.

The problem is that, increasingly, the audience you most need to reach is not there.

Where Gen Z and Gen Alpha Actually Are

Gen Z's oldest cohort turns 30 in 2025. They are not a niche. They are the mainstream consumer for most brands planning the next decade. And 72% of them use ad blockers. Of those who do not, only around one second of attention is the average for a digital ad.

Facebook skews older. Instagram does better with this group but not strongly. TikTok reaches around 60% of Gen Z and 44% of Gen Alpha, the best claim of any platform to this audience.

And yet the number one platform for Gen Z daily time spent is Roblox. Gaming as a category accounts for two hours of Gen Z's daily time. Social media accounts for 1.7.

Something shifted in the mid-2010s and accelerated sharply during lockdown. Gaming was already popular, but Gen Z and Gen Alpha began using gaming platforms as social networks. They were not just there to play. They were there to hang out.

The Attention Economy Has a New Gatekeeper

Every era of media has its gatekeepers. In print, it was Condé Nast. In broadcast, it was Viacom or Comcast. In digital and social, it is Meta, TikTok, X, and Snapchat. These platforms own the audience, and brands pay to access it.

Virtual worlds are no different in principle, but the gatekeepers have changed. The platforms dominating this channel right now are Roblox, with 500 million monthly active users, and Fortnite, with 130 million. Zepeto skews strongly female. More platforms will follow.

Crucially, the model is user-generated content. UGC gaming platforms function the way Instagram and TikTok do: the platform provides the infrastructure, users create the content. For brands, this means low barriers to entry, an existing ecosystem of creators and agencies, shorter lead times, and the ability to build persistent presences without negotiating directly with Roblox or Epic Games. You can go to a creator, go to an agency, and be live in weeks rather than years.

This is fundamentally different from early brand activations in closed games like Pokémon Go. High entry costs, long build timelines, temporary placements, no audience ownership. UGC platforms change that calculus entirely.

Inside Virtual Worlds, Branded Content Holds Attention for Minutes — Not Seconds

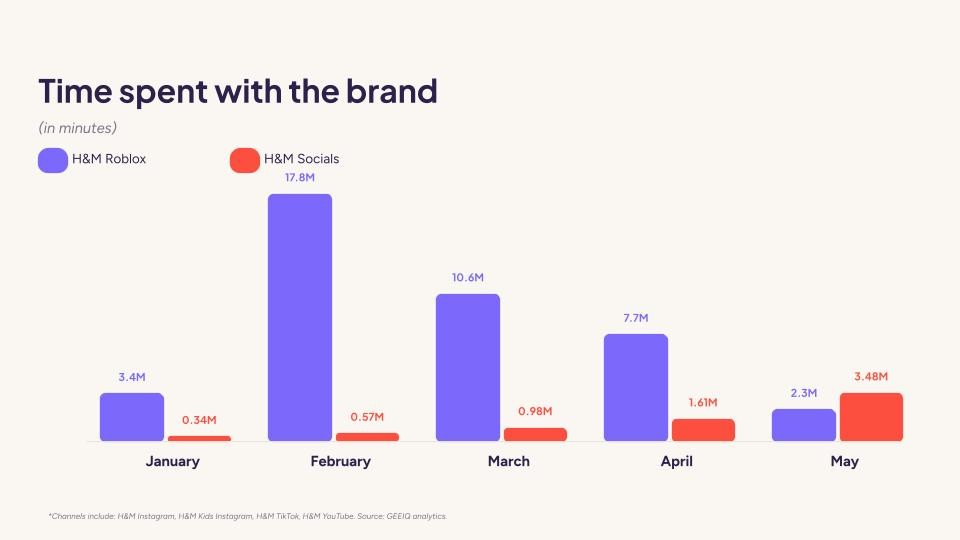

When a user scrolls past branded content on social media, average engagement time is around 1.3 seconds. Inside a branded experience on Roblox, average engagement time is 11 minutes. That is not a marginal difference. It is a different category of attention.

The reason is that virtual worlds are an active experience, not a passive one. Users are inside these environments with their friends. They are making choices, completing activities, spending time with a brand on their own terms. The data from H&M's Roblox world makes this concrete.

The comparison that makes most sense here is not digital advertising. It is experiential marketing: footfall, dwell time, engagement with brand environments, and downstream purchase intent. That is what the measurement actually reflects.

How the Measurement Translates

One concern that comes up when brands first explore virtual worlds is how to present results internally. The metrics look different. The terminology is unfamiliar. That concern is addressable.

Virtual OOH sits on top of verified user data, not modelled estimates. Footfall becomes exact impressions. Dwell time and viewability are measured directly. Integration-based activations, placing a brand inside an existing experience with an established user base, map closely to influencer marketing metrics. Instead of likes, comments, and shares, you measure visits to branded areas, mini-game completions, time spent, and reward redemptions. The measurement architecture is equivalent. The language adapts.

At the owned-world level, the equivalent is building a branded Instagram profile in 3D: persistent, audience-owned, and measurable on the same terms as any owned social channel. And as brands like Walmart have demonstrated, real-world commerce inside these environments is no longer a future possibility.

The Trend Line

GEEIQ tracks every branded activation across UGC gaming platforms. In 2020, there were 180 new brand activations across virtual worlds. In 2025, there were 3,450. The total number is rising. So is the proportion of brands returning for a second activation, which is the more telling figure. Brands that measure are coming back.

The channel is no longer experimental. The measurement frameworks exist. The audience data is there. The question now is whether virtual worlds sit in the marketing mix as a core channel, or whether brands continue leaving those 2.6 daily hours of Gen Z attention to somebody else.

Check out the full talk below 👇

Book a demo with

one of our experts

See how GEEIQ helps brands measure and grow virtual world impact